By Hawk Surveillance Systems, California construction site security Last updated: June 2026

Editorial disclosure: This article is educational and intended for general guidance only. It is not insurance, legal, or financial advice. Hawk Surveillance Systems is not an insurance broker, agent, or carrier. Builders risk policies, mitigation credits, and underwriting practices vary significantly by carrier, project, and state. Always confirm specific policy terms, premium impacts, and acceptance requirements with your licensed insurance broker or agent before making decisions about coverage or site security investment.

Surveillance, Builders Risk, and What Underwriters Actually Reward

A surveillance trailer can be a meaningful factor in a builders risk underwriting conversation, but it does not produce a fixed, advertised “discount” the way some insurance lines do. Underwriters generally evaluate site security as one part of your overall risk profile alongside loss history, project value, location, and construction type.

For California GCs, the practical impact is often less about a visible line-item reduction and more about achieving policy acceptance and reasonable terms in a tight market. That distinction matters. A project that gets written at a workable rate because it presents as a well-managed risk is financially better off than one facing restrictive terms or declination.

Treat this article as a guide to how underwriting actually works and what documentation your broker needs to position your project. Do not treat it as a promise of savings. Your broker remains the only party who can confirm how a specific carrier will respond.

Below: how builders risk underwriting generally works in 2026, what counts as site security to a carrier, and how to package surveillance into a documentation set your broker can use.

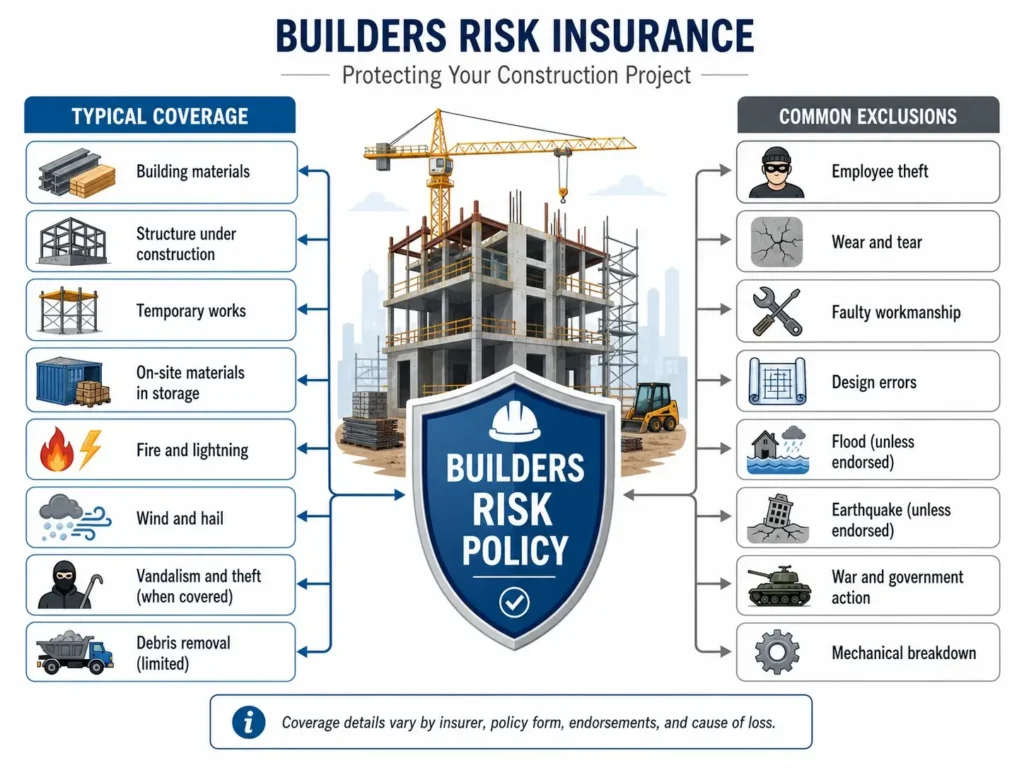

Builders Risk Insurance 101 (For California GCs Who Need a Refresher)

What Builders Risk Covers

Builders risk insurance, often called course of construction insurance, is a specialized property policy that covers a project while it is being built. According to general guidance from the Insurance Information Institute and IRMI, it typically protects the structure under construction, materials stored on-site, and in some cases materials in transit.

Coverage is generally written on a project cost basis, meaning the total insured value reflects the completed value of the build. Depending on how the contract is structured, the policy may be purchased by the owner, the general contractor, or jointly.

Some policies extend to temporary structures such as scaffolding or forms, though this varies. Always confirm scope with your broker because policy language differs across carriers and endorsements.

What Builders Risk Typically Excludes

Most builders risk policies are based on standardized forms developed by organizations like ISO / Verisk, with carrier-specific modifications. Common exclusions often include:

Typical Exclusion | Description |

Employee theft | Internal theft by employees or subcontractors may be excluded |

Faulty workmanship | Defects in design or construction are generally not covered |

Gradual water damage | Slow leaks or seepage are typically excluded |

War and terrorism | Covered only if specifically endorsed |

These exclusions vary significantly. You should review your policy wording with your broker to understand exactly where your exposures sit.

Theft and Vandalism: Where the Coverage Question Gets Real

Theft and vandalism are generally covered perils, but coverage often comes with deductibles, sub-limits, and conditions. High-theft items like copper wiring, appliances, and tools may be subject to tighter terms.

This is where site security becomes financially relevant. If theft losses are frequent in your project class or geography, underwriters typically scrutinize how you are mitigating that risk. Surveillance is not just about preventing loss. It becomes part of how your project is evaluated.

The 2026 Builders Risk Market in California

Hard Market Conditions and Premium Pressure

The builders risk market remains firm in 2026. Industry trade reporting over the past year indicates continued underwriting discipline, with carriers focusing on profitability after several years of elevated loss activity.

For GCs, that generally translates into higher premiums, stricter underwriting, and more documentation requirements. Construction lines have seen meaningful rate increases over recent renewal cycles, with the magnitude varying significantly by risk profile and carrier. Always confirm your specific renewal outlook with your broker.

Theft Loss Trends and Their Underwriting Impact

Construction theft continues to influence underwriting. Industry tracking by the National Insurance Crime Bureau generally shows that construction sites remain frequent targets for theft of materials and equipment.

When loss frequency rises in a category, carriers typically respond by tightening guidelines. That can mean higher deductibles, stricter conditions, or additional underwriting scrutiny. Security measures become part of how underwriters assess whether your project fits within their risk appetite.

Why California Specifically

California presents a unique combination of underwriting challenges:

- High total insured values on urban and infrastructure projects

- Dense jobsite environments with higher theft exposure

- Elevated costs of materials such as copper

- Natural catastrophe exposure, including wildfire and earthquake

Because of this, California projects are often more heavily scrutinized. A documented, credible site security strategy can materially influence how your submission is perceived. Your broker can clarify how this applies to your specific carrier.

For broader context on theft patterns, see our California construction site theft 2026 statistics report.

The Underwriting Factors That Drive Builders Risk Premiums

Project Value, Type, and Duration

Total insured value, construction type, and project timeline are primary rating drivers. A $50M multifamily project over 24 months carries a different exposure profile than a short-term warehouse build.

Higher value and longer duration typically increase premium because they extend exposure to risk.

Location and Crime Exposure

Underwriters generally evaluate location at a granular level. Crime rates, proximity to emergency services, and environmental exposures all matter.

Urban infill sites and remote locations each present different risks. Documenting how you address those risks is critical.

Construction Type and Materials

Wood frame construction, steel, and concrete all carry different risk profiles. Projects involving high-value materials such as copper wiring or finished fixtures often receive additional scrutiny.

Loss History and Claims Experience

Past claims history is generally one of the most influential factors. If your company or project type has experienced theft losses, underwriters will typically look closely at what has changed.

Site Security and Risk Mitigation

Site security is one of several mitigation factors that can influence underwriting. This includes fencing, lighting, access control, and active surveillance.

A documented security approach signals risk awareness and operational discipline. That can be favorable in underwriting, though outcomes vary by carrier and policy. Always review how your specific insurer evaluates mitigation with your broker.

How Site Security Actually Influences Premiums

Mitigation Credits and Schedule Rating

Schedule rating refers to an underwriter’s ability to adjust a premium up or down within a defined range based on qualitative factors. IRMI generally notes that this can include elements like management practices and risk controls.

Site security can be one of those factors. However, it is not a fixed or published discount. It is part of a broader evaluation.

What Counts as “Site Security” to an Underwriter

Underwriters generally look for layered security:

Layer | Example |

Perimeter | Fencing, barriers |

Lighting | Adequate illumination |

Access control | Controlled entry, logs |

Surveillance | Cameras with monitoring |

Response | Documented incident procedures |

A single camera without monitoring rarely carries weight. A documented system with active oversight is generally more meaningful.

The Difference Between a Discount and an Acceptance Decision

This is the most important distinction. In many cases, security does not translate into a visible discount. Instead, it can influence whether a project is accepted and under what terms.

💬 Hawk Insight: Underwriters rarely advertise specific discounts for surveillance. They evaluate the full risk profile and decide whether to write the policy and at what terms. Strong documentation can move your project toward acceptance and more reasonable conditions, but the actual outcome is always determined by the underwriter and disclosed by your broker.

What a Site Security Plan Looks Like (And Why Underwriters Ask For One)

The Five Components of a Defensible Security Plan

A defensible site security plan generally addresses five layers:

- Perimeter; fencing, barriers, controlled boundaries

- Lighting; night visibility across high-value zones

- Access control; entry tracking and visitor logs

- Surveillance; cameras with active monitoring

- Incident response; documented procedures and contacts

Underwriters typically want to see how each layer is addressed, who is responsible, and what documentation backs the plan.

Documentation, Photos, and Evidence of Active Monitoring

Underwriters generally do not rely on verbal assurances. They expect documentation. That includes photos, equipment specs, monitoring agreements, and incident logs.

How Surveillance Trailers Fit Into the Plan

Surveillance trailers address active monitoring and response in a portable format. For temporary jobsites, they can provide a documented layer of protection that can be deployed quickly. Combined with 24/7 remote monitoring, they support the surveillance and response layers of a defensible plan.

Your broker can advise how to present this documentation during underwriting.

💬 Hawk Insight: When a carrier looks at a “site security” answer, they are looking for evidence, not assertions. A trailer with documented camera specs, a monitoring agreement, and an incident response procedure tells a different story than a sentence on a submission saying “site has cameras.”

The Documentation Packet: What to Bring to Your Broker

Equipment Specifications and Coverage Maps

Detailed specs, camera capabilities, and coverage diagrams help underwriters understand how the site is monitored.

Monitoring and Response Protocols

24/7 monitoring agreements, response procedures, and escalation steps demonstrate active oversight.

Incident Response and Documentation Procedures

Clear processes for documenting and sharing incidents strengthen your risk profile.

Certificates of Insurance from Your Security Vendor

Vendors providing security services often supply their own COI, which underwriters may request.

💬 Hawk Insight: When we deliver a quote, we include a documentation packet your broker can use. We do not determine insurance outcomes. We provide the clearest possible file for underwriting review.

Send your project details. We return a configuration recommendation, a deployment cost estimate, and a documentation packet your broker can use during your builders risk renewal conversation.

Three California Scenarios Where Surveillance Made the Underwriting Conversation Easier

The following are illustrative scenarios. Actual underwriting outcomes depend on the specific carrier, broker, project, and risk profile.

Scenario 1: A $50M Bay Area Multifamily Project

A multifamily build at $50M with a 24-month schedule combines extended timeline exposure with high-value materials, including copper and finished fixtures. Documented surveillance with 24/7 monitoring and a defined incident response procedure gave the broker concrete evidence to support the underwriting submission. The coverage was bound at terms the GC and owner could underwrite to, with a documented site security plan included in the renewal file for the second year.

Scenario 2: A Central Valley Logistics Build with Prior Theft Losses

A logistics warehouse build with prior copper and equipment theft losses faced stricter scrutiny at renewal. The team added a documented surveillance trailer deployment, a monitoring agreement, and an incident logging protocol. The underwriter accepted the project at terms that would not have been available without documented mitigation. The premium did not drop, but the carrier wrote the policy where another carrier had previously declined.

Scenario 3: A Sacramento Public Works Project Requiring 24/7 Coverage

Some public works contracts include security and surveillance requirements. The same documentation that satisfied the contract also supported the builders risk submission. The broker used the surveillance documentation to address mitigation in the underwriting file, simplifying the conversation with the carrier.

Send your project details and your broker’s contact information. We return a configuration recommendation and a documentation packet your broker can use in their underwriting conversation.

What to Ask Your Broker This Week

Five questions to take to your next broker conversation:

- Does our builders risk policy consider site surveillance as a mitigation factor?

- What documentation is required from our security vendor?

- Are there endorsements related to monitoring or security plans?

- How does theft deductible structure interact with mitigation?

- How does our loss history impact underwriting, and can security offset it?

Your broker is the only party who can provide binding answers.

Frequently Asked Questions

Do surveillance trailers lower builders risk insurance premiums?

Surveillance trailers may influence underwriting, but they do not create guaranteed premium reductions. They can support mitigation discussions and improve how a project is evaluated. Outcomes depend on the carrier, policy, and risk profile. Always confirm with your broker.

What is builders risk insurance and what does it cover?

Builders risk insurance covers a project during construction, including structures and materials. It is generally written on a project value basis. Coverage varies by policy, so confirm details with your broker.

Does builders risk insurance cover theft and vandalism?

Builders risk policies often include theft and vandalism, but with conditions and limits. High-value items may have sub-limits. Review your policy with your broker for specifics.

What underwriting factors influence builders risk premiums in California?

Premiums are typically influenced by project value, location, construction type, loss history, and risk mitigation. Each factor is generally evaluated by the underwriter as part of an overall risk profile.

How much can site security reduce my builders risk premium?

The impact varies significantly by carrier, project, and risk profile. Security may support mitigation credits or acceptance decisions. Your broker can explain how it applies to your policy.

What is a security plan and why do underwriters ask for one?

A security plan documents how a site is protected. Underwriters generally use it to assess risk management practices and exposure.

Will my carrier require surveillance for high-value projects?

In some cases, carriers may require documented security measures for high-value or high-risk projects. Requirements vary, so consult your broker.

What documentation does a broker need to apply security as a mitigation factor?

Documentation typically includes equipment specs, monitoring agreements, photos, and incident procedures. Your broker will specify what is needed for your specific carrier.

Can surveillance footage help resolve a builders risk claim faster?

Footage can support claims documentation and clarify events. Its impact depends on the claim and carrier handling.

Does Hawk Surveillance provide insurance documentation for our broker?

Yes. Hawk provides a documentation packet with quotes that brokers can use during underwriting discussions. We do not provide insurance advice. We provide the documentation your broker requests.

Key Takeaways

- Builders risk insurance varies widely by carrier and project

- California projects face heightened underwriting scrutiny in the current market

- Site security is a mitigation factor, not a guaranteed discount

- Acceptance and terms often matter more than visible premium reductions

- Documentation is critical in underwriting

- Surveillance trailers support a defensible security plan when paired with monitoring and incident response

- Your broker is the final authority on outcomes

Get a Quote with Insurance Documentation Packet

Send us your project details and your broker’s contact information. We will return a configuration recommendation, a deployment cost estimate, and a documentation packet your broker can use during your builders risk renewal conversation. Hawk does not give insurance advice. We provide the documentation your broker needs.

This guide is educational. It is not a promise of premium reduction, a guarantee of policy acceptance, or a substitute for advice from your licensed insurance broker. Always confirm specific policy terms, mitigation credits, and underwriting requirements directly with your broker or carrier before making decisions about coverage or site security investment.